An education loan is a blessing for all those students who cannot afford the exponentially rising cost of higher education. And, it’s for the scholars whether studying in India or abroad. There are multiple leading private sector and public sector banks as well as NBFCs that offer education loans today. And, getting an education loan today may have become easier. Still, choosing the right kind of education loan is still quite complex a process. Here, we shall discuss some tips on helping our readers select the best education loan for their studies abroad.

{kind=link}

Eligibility for Education Loans

Before moving ahead with the best education loan for abroad studies, let us first take a look at the basic eligibility criteria that students need to fulfill for being eligible to get an education loan. Most banks have their unique eligibility criteria which differ from case to case. We, therefore, list down a few basic criteria that are needed by most leading banks.

- The students applying for an education loan must be a citizen of India.

- The student must have gained confirmed admission to a job-oriented program in an educational institute in India or abroad. The institute must be approved or recognized by relevant authorities.

- Students who take an education loan for pursuing a full-time program must have a co-applicant. The parent or guardian or spouse (in case of married students) can be the co-applicant.

- Students applying for an education loan must have a good academic record.

- Students should also check their and their co-applicants’ CIBIL score before applying.

Once students have ensured that they meet the basic eligibility requirements for an education loan, they can start looking for the best bank.

Successful meeting of the basic eligibility requirements by the students will result in their search for the best bank.

To determine this, students should keep a few points, listed below, in mind.

Economic Factors

When planning to take an education loan, students should consider economic factors first. Under this, there are certain points that should be kept in mind before taking the final call. These are as following:

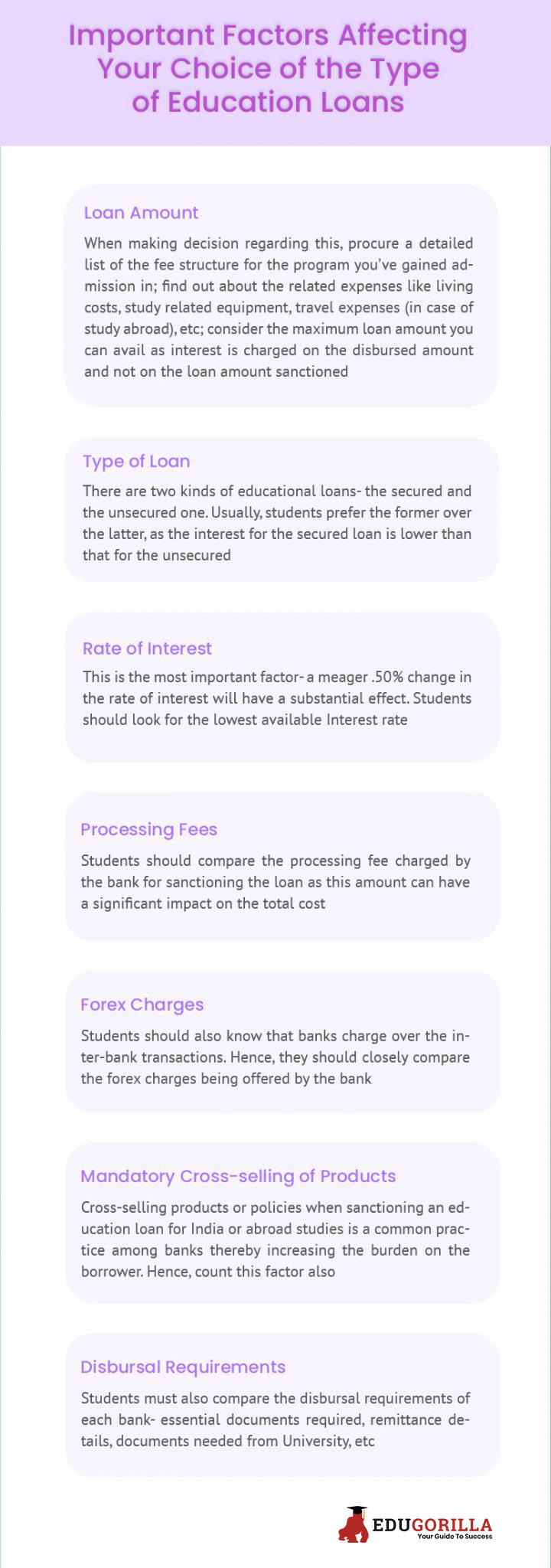

Loan Amount

This is the first thing that students must consider when applying for an education loan. Students should first procure a detailed list of the fee structure for the program they have gained admission in. They should also find out about the related expenses. These expenses are such as living costs, study related equipment, travel expenses (in case of study abroad), etc. Knowing about the approximate amount that they must pay for the program, they can consider the loans available to them. Students should look for the maximum loan amount that the bank can sanction. This is because interest is charged on the disbursed amount and not on the loan amount sanctioned. The maximum loan amount also helps in meeting unexpected expenses.

Type of Loan

Students may finalize the loan amount. Still, they should look at the type of loan that the bank offers for their requirement. Banks basically provide two types of loan – a secured loan and an unsecured loan. A secured loan is a loan in which the bank needs the borrower to attach security with the loan. The bank can use the tangible collateral (a property, fixed deposit, insurance policy, etc.) when non-repayment of the loan occurs. An unsecured loan, on the other hand, needs no collateral and only requires the income proof of co-applicant.

Readers should always prefer a loan with collateral over an education loan for India or abroad studies without collateral. This is because the interest for a secured loan is always lower than for an unsecured loan. Moreover, it has no repayment during the study period. Still, a secured loan may not be available to the students. Hence, they can always opt for education loan for India or abroad studies without collateral.

Rate of Interest

The interest rate being charged by the bank is one of the most important criteria that students should look at before selecting the bank for an education loan for abroad studies. Even a meager .50% change in the rate of interest will have a substantial financial effect. Students should look for the lowest available Interest rate. They can take the help of GyanDhan’s tool, EMI Calculator to understand the economic impact that the rate of interest will have. If students have a hard time choosing between an education loan in USD with a lower interest rate and an education loan in INR with a higher rate of interest, we suggest selecting the one in INR, keeping in mind the previous trends that point towards a higher rate of conversion from USD to INR.

Processing Fees

Once students have decided on a couple of prospective education loan for studying in India or abroad, they should compare the processing fee charged by the bank for sanctioning the loan as this amount can have a significant impact on the total cost. For example, NBFCs charge around 1% of the total loan amount as a processing fee. Hence, any reduction in the processing fee is beneficial to the borrower.

Forex Charges

Students should also know that banks charge over the inter-bank transactions. Hence, they should closely compare the forex charges being offered by the bank and look for one which suits your requirements or offers a live rate and thus hedges amidst market fluctuations.

Mandatory Cross-selling of Products

Cross-selling products or policies when sanctioning an education loan for India or abroad studies is a common practice among banks. For example, some banks might try to sell a mutual fund scheme when sanctioning an education loan. However, this increases the burden on the borrower. Students must, therefore, consider this, before taking an education loan.

Disbursal Requirements

Students must also compare the disbursal requirements of each bank. This includes comparing the essential documents required, remittance details, documents needed from University, etc.

Utilization of the Loan

When considering various banks for the best education loan, students must also consider how, and for which purpose they will be using the funds and whether their lender allows for the same. For example, some lenders might not cover the associated costs of the program, such as a library fee or laboratory fee, etc. So, students should compare these before finalizing their education loan.

Tenure of the Loan

Tenure of the loan is another important factor to compare when taking an education loan. In some cases, the initial average compensation after completing a certain course is not adequate to repay the education loan in a short period of time, in such cases; long tenure eases the burden of high EMIs. Long tenure is anyway an effective hedging method in the unpredictable job market.

Repayment

Students should also keep an eye on the repayment clauses of their education loan. During the moratorium period, students are exempt from repayments. This is highly beneficial as students do not have to worry about repaying while studying. Hence, students should take this into consideration.

Check for Banks That are in Liaison with Your University for Concessions

Some of the leading lenders in India recognize some universities land and have a student loan liaison with these universities. When students take a loan from such banks that have liaison with their university, the chances of getting their loan sanctioned is higher. Find out about this before taking an education loan.

NBFCs such as Avanse and Incred and private and public sector banks such as ICICI, AXIS, & BoB and SBI provide education loans to deserving students at competitive rates of interest. Students can approach these banks to avail an education loan. Alternatively, they can also take the help of GyanDhan – India’s first education-focused financing platform and know about their loan eligibility as well as get help in getting their loan sanctioned.

{kind=link}

With their fast and simple education loan process, students can get their loan sanctioned from three to twelve working days depending on the type of Lending agency. They not only match your profile with leading lenders in the country and help select the best loan possible, but also help with document submission, and in following up with the lenders. They even coordinate the loan disbursal according to the schedule of your University.

Getting an education loan is no rocket science in today’s times. However, selecting the correct education loan needs meticulous planning and research and can help reduce the overall cost by several lakhs. So, follow the above steps and select the best education loan for yourself or take the help of GyanDhan now.

You Might Want To Read:

Social Work Question Paper 4 2011, Nmat Eligibility Criteria, Aakash Institute Vs Allen Institute, Cet Cet Mock Question Paper 2 2, Budget 2019 Wishlist For The Education Sector, Sentence Shifting, Root Words, General Science Technology, City Kanpur, University Entrance Examination

Leave your vote

This post was created with our nice and easy submission form. Create your post!